Best Jurisdictions for Real Estate Tokenization in 2025

Key Takeaways

- The Middle East, led by the UAE, is emerging as the global leader in real estate tokenization thanks to cohesive government backing and clear legal frameworks.

- Asia Pacific is rapidly scaling, driven by regulatory clarity in Singapore, Thailand, and Japan, but uneven adoption across the region creates execution asymmetry.

- The U.S. offers scale and innovation and is now showing early signs of regulatory progress, though uncertainty and compliance friction continue to limit mainstream adoption.

- The EU has a mature legal foundation but faces challenges from regulatory fragmentation, risk-averse positioning, and low capital deployment.

4 Regions: Let us compare

We believe real estate tokenization is reshaping access to property markets, but not all regions are moving at the same pace. This article provides a clear, comparative framework for evaluating global readiness. Our analysis covers the United States, European Union, Asia Pacific, and the Middle East across six performance indicators, helping institutional stakeholders, asset managers, and policy leaders navigate where opportunity meets execution.

Part 1: The Global Scorecard For Real Estate Tokenization

The Middle East is setting a new benchmark with government-led initiatives, legal clarity, and billion-dollar tokenization deals. Asia Pacific is close behind, with high activity in Singapore, Thailand, and Japan. The U.S. continues to dominate in volume and innovation but struggles with regulatory inconsistency. The EU remains cautious, well-regulated, but fragmented and slow to scale.

Asia Pacific 4/5⭐️

Asia Pacific is becoming one of the most active and forward-thinking regions for tokenized real estate. Singapore, Thailand, and Japan lead the way.

Flagship examples include Thailand’s SiriHub tokenization of a commercial building, CitaDAO’s tokenized industrial assets in Singapore, and Japan’s multi-hundred-million-dollar security token issuances. Elevated Returns has launched cross-border offerings in Thailand, while Hong Kong and South Korea are expanding retail access to tokenized RWAs.

The region has avoided scandals thanks to tight regulatory controls. Most issuances are overseen by national financial authorities and follow securities law.

Tokenized real estate in the region exceeds one billion dollars, led by Japan and Thailand. Volumes are increasing steadily, particularly in institutional markets.

Regulatory and government support is strong. Singapore’s MAS operates Project Guardian and licenses platforms like ADDX and InvestaX. Thailand has created a bespoke legal regime. Japan and Hong Kong are expanding retail tokenization permissions. While some ASEAN countries are lagging, the region’s leaders offer blueprints for secure and scalable tokenization.

Industry activity is dynamic. Regional exchanges, fintechs, and traditional banks are all active. Global players are entering through hubs like Singapore and Tokyo.

Strategic positioning: Asia Pacific combines policy leadership with commercial execution, making it a high-growth zone for tokenized real estate.

Middle East 4.6/5⭐️

The Middle East, particularly the UAE, has become a global benchmark for real estate tokenization, thanks to cohesive public-private coordination and proactive legal reforms.

Flagship projects include MAG Group’s three-billion-dollar tokenization of luxury properties in Dubai, a pilot by the Dubai Land Department integrating title deeds on blockchain, and active development from Damac Properties and others.

No scandals have been reported. All initiatives are tightly supervised by authorities like VARA and DLD, ensuring transparency and compliance.

Tokenized assets in the region now exceed several billion dollars, with clear growth targets including a 16 billion dollar roadmap by 2030. The UAE has moved from pilot to institutional scale faster than any other jurisdiction.

Regulatory and government support is exceptional. Dubai created dedicated legislation, formed VARA, and integrated blockchain into official registries. Abu Dhabi and Bahrain are also building compliant frameworks with dedicated sandboxes.

Strategic positioning: The Middle East is executing tokenization at scale through coordinated regulation, infrastructure, and capital.

European Union 2.8/5⭐️

The EU offers legal maturity and clear definitions for digital securities in several member states. However, regional fragmentation and cautious regulators slow the pace of tokenized real estate adoption.

Flagship use cases include tokenized bond structures in Germany via the eWpG law, STOKR’s cross-border issuances, Reental’s growing portfolio in Spain, and BrickMark’s high-value commercial property tokenization in Switzerland.

Scandals are absent, but risks remain. In September 2025, ESMA warned that tokenized instruments may mislead investors about rights and protections, flagging the need for stronger safeguards.

The EU’s tokenized real estate market remains small, with total value under 200 million euros.

Regulatory and government support is structured but uneven. Initiatives like the DLT Pilot Regime, Germany’s eWpG, and France’s Pacte law provide clarity. Still, no unified EU-wide regime exists for security tokens.

Industry activity is moderate. Firms like Tokeny, Black Manta Capital, and Reental are active, as are a few traditional banks. However, risk-averse postures and fragmented oversight limit institutional engagement.

Strategic positioning: The EU is legally mature but operationally fragmented and risk-sensitive.

United States 3.8/5⭐️

The United States combines deep capital markets, institutional firepower, and fintech innovation, making it a hotspot for tokenization pilots. While historically constrained by a lack of federal regulatory clarity, 2025 has seen early signs of change. The House-passed CLARITY Act proposes a clearer jurisdictional split between the SEC and CFTC, and the SEC’s Project Crypto signals support for modernized digital asset classification, tokenized securities issuance, and integrated market infrastructure.

Flagship use cases include the St. Regis Aspen Resort tokenization, fractional property platform RealT, the DAO-structured Immaculata Living development in Chicago, and the MAGMA pilot in Miami integrating digital twin infrastructure across 40 live buildings. These illustrate both institutional and retail interest in tokenized real estate.

Failures include enforcement actions against fraudulent schemes like RECoin and Unicoin, and operational breakdowns in RealT’s Detroit portfolio. Despite these, many projects operate within legal exemptions (Reg D, Reg S), maintaining investor protections.

The U.S. commands the largest global share of tokenized real estate but it remains a fraction of the $17 trillion commercial property market.

Regulatory and government support is improving but still fragmented. States like Wyoming continue to push tailored legislation. The SEC’s roundtable on tokenization and new policy initiatives mark a shift toward engagement, but federal implementation remains incomplete and compliance burdens persist.

Industry activity is unmatched. Startup ecosystem is joined by major institutions including BlackRock, Franklin Templeton, and JPMorgan. However, most remain in pilot mode, awaiting further regulatory clarity.

Strategic positioning: The U.S. leads in innovation and scale and is now showing the first signs of coordinated regulatory progress.

Part 2: Regulatory Modus Operandi by Region

When tokenizing a real estate fund, stakeholders must navigate a complex web of legal and procedural checkpoints across the asset lifecycle. Below, we outline how each major region addresses the key touchpoints in that journey, from fund formation to cross-border distribution. As our CEO, Rachid Ajaja, puts it:

"Tokenization itself is not the hard part. It is navigating the regulatory maze and selecting the right legal framework that determines success."

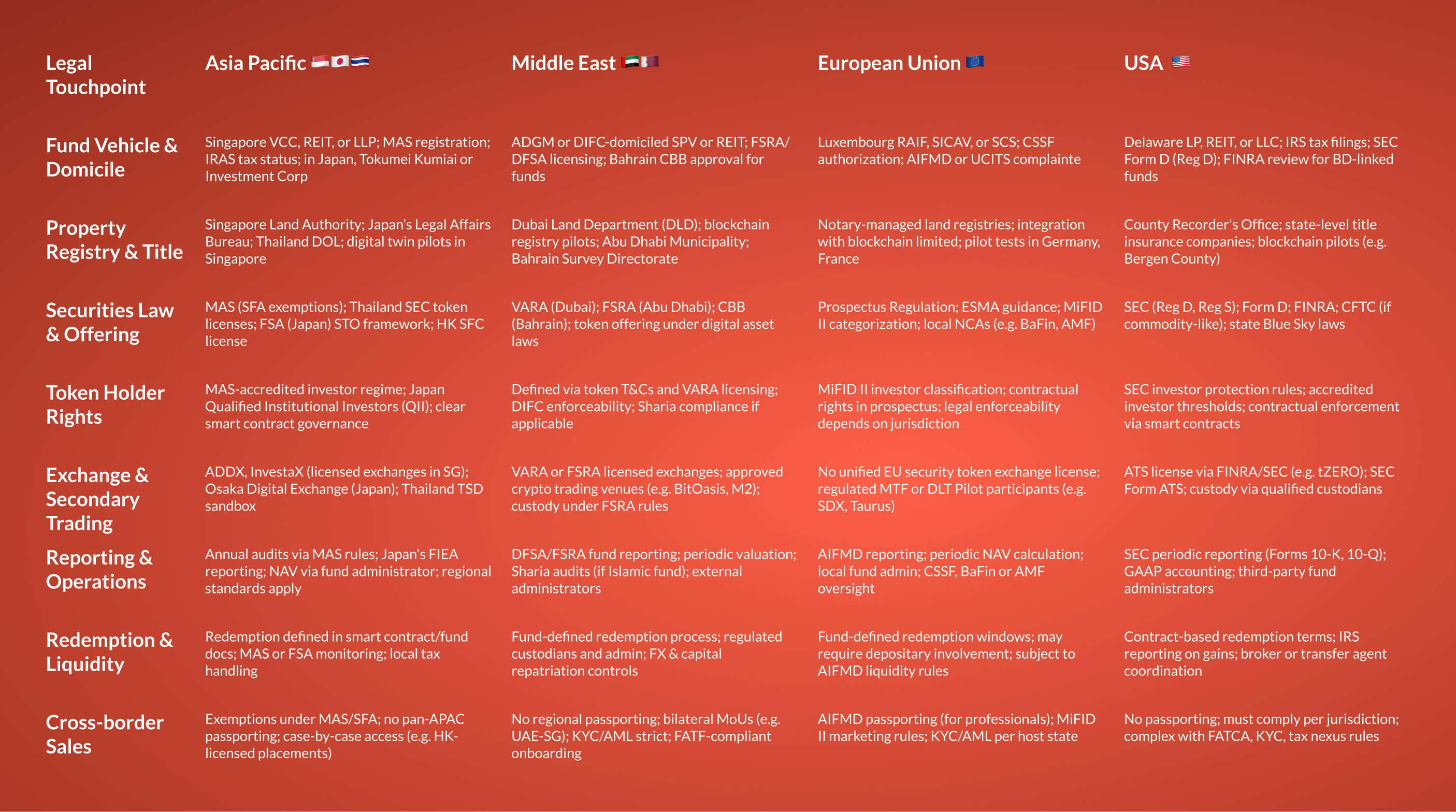

Asia Pacific 🇸🇬🇯🇵🇹🇭

Fund Vehicle & Domicile: Singapore offers VCCs, REITs, or LLPs. In Japan, structures like Tokumei Kumiai are common. Registration with MAS, FSA, or IRAS may be required depending on the structure.

Property Registry & Title: Managed by public agencies like the Singapore Land Authority, Japan’s Legal Affairs Bureau, and Thailand’s Department of Lands. Digital twin trials are active in several cities.

Securities Law & Offering: MAS (Singapore), FSA (Japan), and SEC (Thailand) oversee token offerings. Most projects operate under exemptions or sandbox programs. Hong Kong requires SFC licensing.

Token Holder Rights: Jurisdictions classify investors (e.g., QIIs in Japan, accredited investors in Singapore). Rights and voting logic can be embedded in smart contracts.

Exchange & Secondary Trading: Licensed exchanges like ADDX and InvestaX (Singapore), Osaka Digital Exchange (Japan), and sandboxed venues in Thailand offer trading infrastructure.

Reporting & Operations: Annual audits, NAV calculations, and operational disclosures are mandated by regional regulators (e.g., MAS, FSA, IRAS).

Redemption & Liquidity: Redemptions are handled via smart contracts and fund rules. Compliance oversight comes from MAS or equivalent.

Cross-border Sales: No regional passporting. Case-by-case exemptions apply. KYC/AML depends on host state rules.

Middle East 🇦🇪🇶🇦

Fund Vehicle & Domicile: Vehicles are domiciled in ADGM or DIFC with licensing from FSRA or DFSA. Bahrain uses CBB-regulated fund structures.

Property Registry & Title: Managed by entities like the Dubai Land Department and Abu Dhabi Municipality. Dubai is piloting blockchain-based registries.

Securities Law & Offering: Governed by VARA (Dubai), FSRA (Abu Dhabi), or CBB (Bahrain). Digital asset laws define issuance procedures.

Token Holder Rights: Enshrined in token terms and licensed by VARA or FSRA. Enforceability applies under DIFC law. Sharia compliance is required for Islamic funds.

Exchange & Secondary Trading: Regulated crypto venues like BitOasis and M2 operate under VARA and FSRA. Custody must meet FSRA standards.

Reporting & Operations: Regular reporting is required. Funds undergo valuation cycles and Sharia audits where applicable.

Redemption & Liquidity: Custodians and admins handle fund-defined redemption processes. FX repatriation and capital controls may apply.

Cross-border Sales: No regional passporting. Distribution occurs via bilateral MoUs. FATF-aligned KYC/AML is strictly enforced.

European Union 🇪🇺

Fund Vehicle & Domicile: Common structures include RAIFs, SICAVs, and SCSs (often in Luxembourg). Authorization by local regulators (CSSF, AMF, etc.) and compliance with AIFMD or UCITS is required.

Property Registry & Title: Land registries remain paper-based and notary-managed in most countries, though pilot programs exist in Germany and France for digital integration.

Securities Law & Offering: Governed by the EU Prospectus Regulation, MiFID II, and national competent authorities (e.g., BaFin, AMF). ESMA provides overarching guidance.

Token Holder Rights: Outlined in the fund prospectus. MiFID II defines investor types. Rights enforcement depends on local legal systems.

Exchange & Secondary Trading: No unified security token exchange license yet. MTFs and participants in the DLT Pilot Regime (e.g., SDX, Taurus) are primary venues.

Reporting & Operations: AIFMD requires periodic reporting. Fund NAVs are calculated via approved administrators. Oversight by national regulators like CSSF and BaFin.

Redemption & Liquidity: Defined in fund documentation, often with lock-up periods. Deposit banks may be required. AIFMD imposes liquidity controls.

Cross-border Sales: AIFMD passporting enables EU-wide marketing to professional investors. Retail access governed by MiFID II and local KYC rules.

United States 🇺🇸

Fund Vehicle & Domicile: Delaware LPs, REITs, or LLCs are the standard choices. Regulatory obligations include IRS tax filings, SEC Form D filings for exempt offerings under Reg D, and potential FINRA oversight for broker-dealer-linked structures.

Property Registry & Title: Ownership and title are managed at the county level through Recorder’s Offices. Some states, such as New Jersey, have initiated blockchain-based pilots.

Securities Law & Offering: The SEC regulates tokenized offerings under Reg D (private placements), Reg S (offshore), and occasionally the CFTC (commodities). Blue Sky laws apply state-by-state. Filing a Form D is mandatory.

Token Holder Rights: Governed by SEC investor protection rules and smart contract enforcement. Investors must meet accredited criteria; contractual clarity is essential.

Exchange & Secondary Trading: Trading typically occurs on FINRA- and SEC-licensed Alternative Trading Systems (ATS), such as tZERO. Custody must be handled by qualified custodians.

Reporting & Operations: Periodic reporting (10-K, 10-Q) is required. GAAP standards apply. Fund admins handle NAV and compliance.

Redemption & Liquidity: Redemption logic is embedded in fund docs and smart contracts. Coordination with brokers or transfer agents is required for execution and IRS reporting.

Cross-border Sales: No passporting. Each jurisdiction requires separate compliance with FATCA, local tax laws, and KYC/AML protocols.

Tokenization is no longer a technological question

It is a regulatory one.

Across jurisdictions, the quality of legal frameworks and public-private collaboration is what now determines the pace and scale of adoption. As the comparative analysis shows, regions like the UAE and Singapore have created predictable pathways that balance innovation with investor protection, while legacy markets like the U.S. and EU struggle with regulatory fragmentation or inertia.

For portfolio managers considering tokenizing a real estate fund, the optimal jurisdiction is not just the one with the most capital or liquidity, but the one that enables compliant operations, cross-border scalability, and clear investor rights. Regional strengths vary: the Middle East leads in cohesive frameworks and execution speed; Asia Pacific in sandbox-enabled experimentation; the U.S. in volume and innovation; and the EU in legal maturity.

In this environment, the strategic play is not "if" but "where and how".

Regulatory clarity is the new competitive advantage. Those who understand the procedural landscape and align with the right jurisdictional logic will not only reduce legal risk, but unlock true operational scale for tokenized real estate strategies.